Whatever You Do, Don’t Ignore Friday’s Selloff

Submitted by QTR’s Fringe Finance

By 1PM Friday, the Nasdaq was already down roughly 3.3%, and suddenly the same crowd that spent the last few months explaining why valuations don’t matter is asking what is happening.

Bitcoin has also been taken behind the woodshed, crashing to around $60,000. Depending on where you’re measuring from, that’s a brutal decline in a remarkably short period of time. It’s down about 42% over the last twelve months. And it’s becoming clear that bitcoin bulls all have breaking points.

And I don’t want to sound like a d*ck, but frankly, none of this — the market tanking, or how it’s happening — is really surprising.

I’ve written for years that I think crypto is the tip of the risk-on spear. It tends to be the first asset class investors pile into when liquidity is abundant, speculation is rampant, and everyone is convinced they’re smarter than the market. It’s also frequently the first thing to crack when risk appetite begins to fade. So I’m not terribly surprised that after bitcoin started crashing (it’s down 16% in the last 5 days) that the rest of the market is following suit.

Back in October, crypto was one of ten areas of the market that I flagged as deserving extra caution. I’d be paying very close attention to the other nine areas right now. Markets rarely isolate their problems to one corner of the casino for very long.

The question investors are already asking is predictable: “Is this a buy-the-dip opportunity?”

Maybe, if the rules of economics and markets as we once knew them cease to exist any longer, but let’s not confuse a 3% decline with anything resembling an attractive valuation. Here’s a couple quick notes for perspective on where we are heading into the weekend.

Friendly reminder for those who think this is a “crash” that in 2023, barely 3 years ago, the NASDAQ was more than -59% lower from here.

The current Shiller CAPE ratio sits at 42.7x, a level that should make investors uncomfortable. Historically, the CAPE has averaged just 17.38x, with a median reading of 16.09x, meaning today’s valuation is more than double what investors have typically paid for earnings over the last century.

Even more striking, the market is now approaching the most expensive levels ever recorded. The all-time high was 44.19x at the peak of the dot-com bubble in December 1999, a period not exactly remembered for rational pricing or stellar forward returns.

In other words, despite today’s selloff, stocks remain priced near some of the richest valuations in modern financial history. A 3% decline may feel dramatic on social media, but it barely registers as a scratch when viewed against the backdrop of historically extreme valuations.

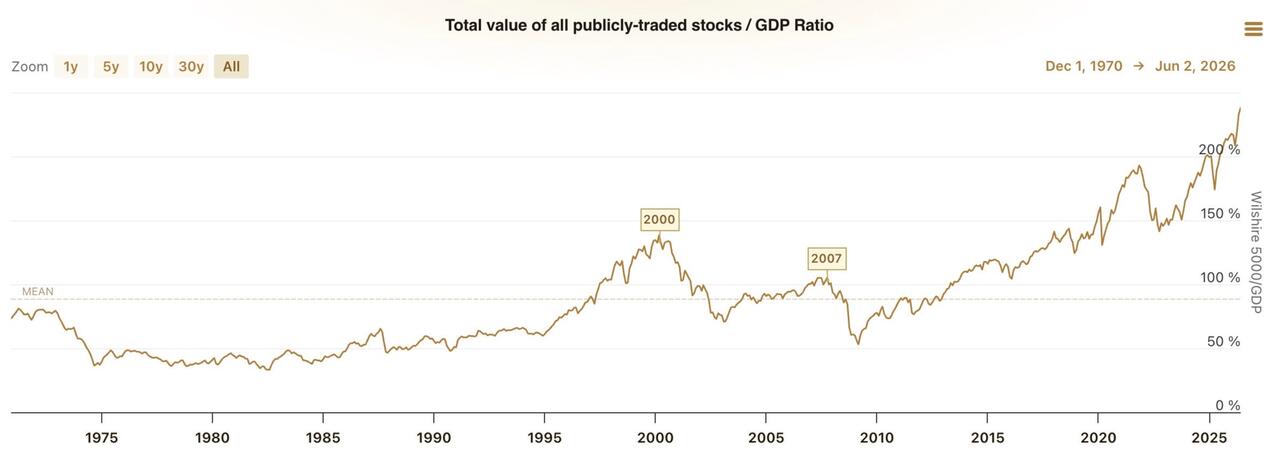

The Buffett Indicator isn’t offering much comfort either. The total value of the U.S. stock market currently stands at roughly $75.4 trillion versus annualized GDP of approximately $31.8 trillion. That places the Buffett Indicator at 237%.

Historically, levels this elevated have been associated with investors discovering, sometimes painfully, that valuation eventually matters. Others, who aren’t in on the Fed-created “good macro news is bad news for markets because rate cuts are less likely” logic—a totally backwards, Jedi-mind-f*ck-deluxe recalibration of economic reality—don’t even seem to consider valuation.

And the uncomfortable reality is that many other investors are still operating under the assumption that the Federal Reserve will ride in on a white horse if markets get into trouble.

That assumption may be outdated. As I’ve written about, it appears the Fed has a problem. Inflation remains stubbornly elevated. Policymakers know financial conditions are tight enough to hurt growth but not loose enough to declare victory on prices. Cutting aggressively risks reigniting inflation pressures. Staying restrictive risks slowing the economy further. In short, the Fed is stuck.

For most of the last fifteen years, every meaningful market decline came with an expectation that central bankers would eventually step in with lower rates, more liquidity, or some variation of monetary painkillers. Today, that safety net looks considerably thinner.

The market may desperately want a rescue eventually, and inflation may not allow one. That creates a setup investors haven’t had to navigate in a long time.

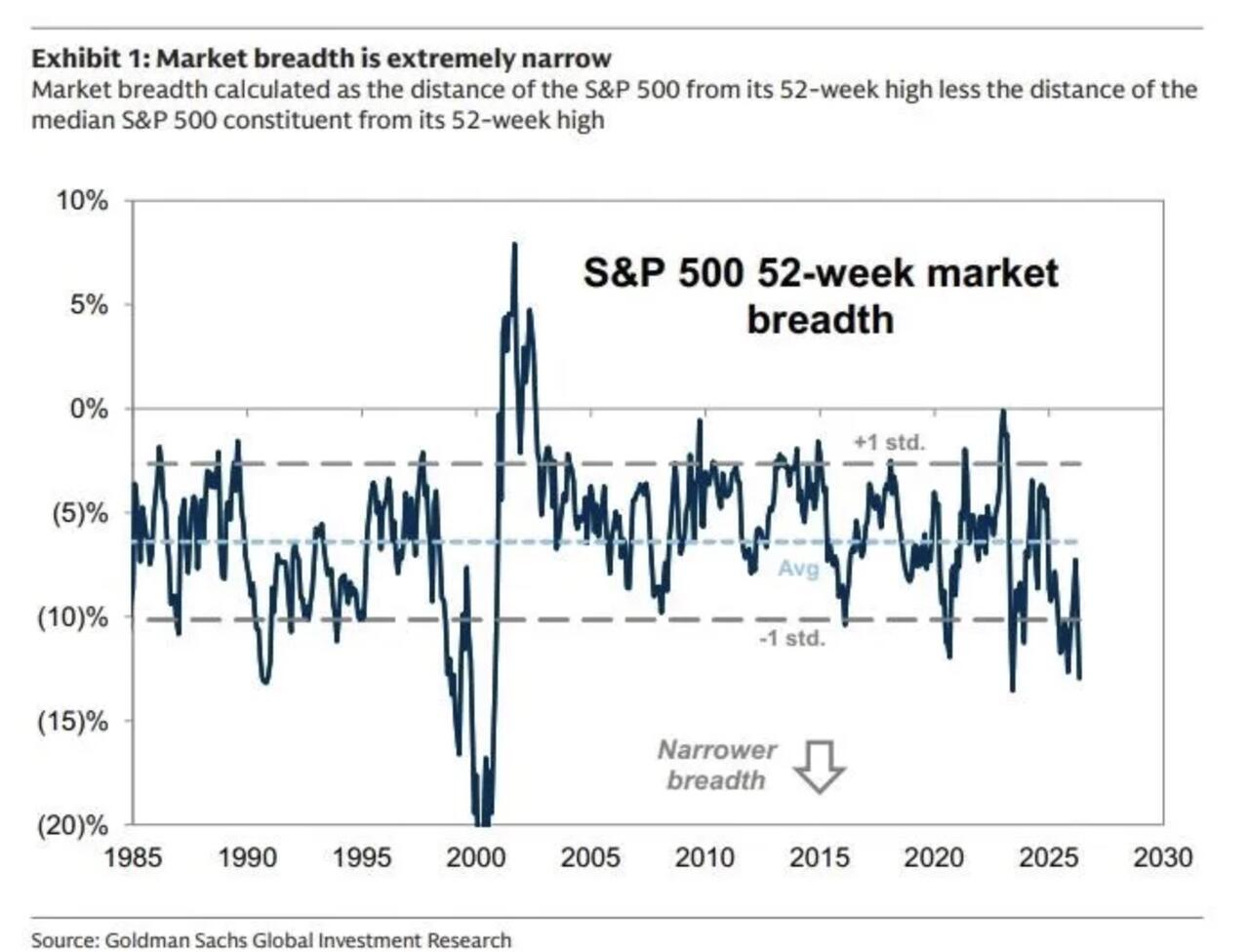

Adding to the risk is the increasingly fragile nature of this rally.

Beneath the headline indexes, breadth has been far less impressive than the bulls would like to admit. A relatively small number of stocks have been doing a disproportionate amount of the heavy lifting. This is why I wrote the other day that investors in the SPY may want to also inform themselves about the RSP ETF — which is equal weighted — if they want to stay in the market going forward.

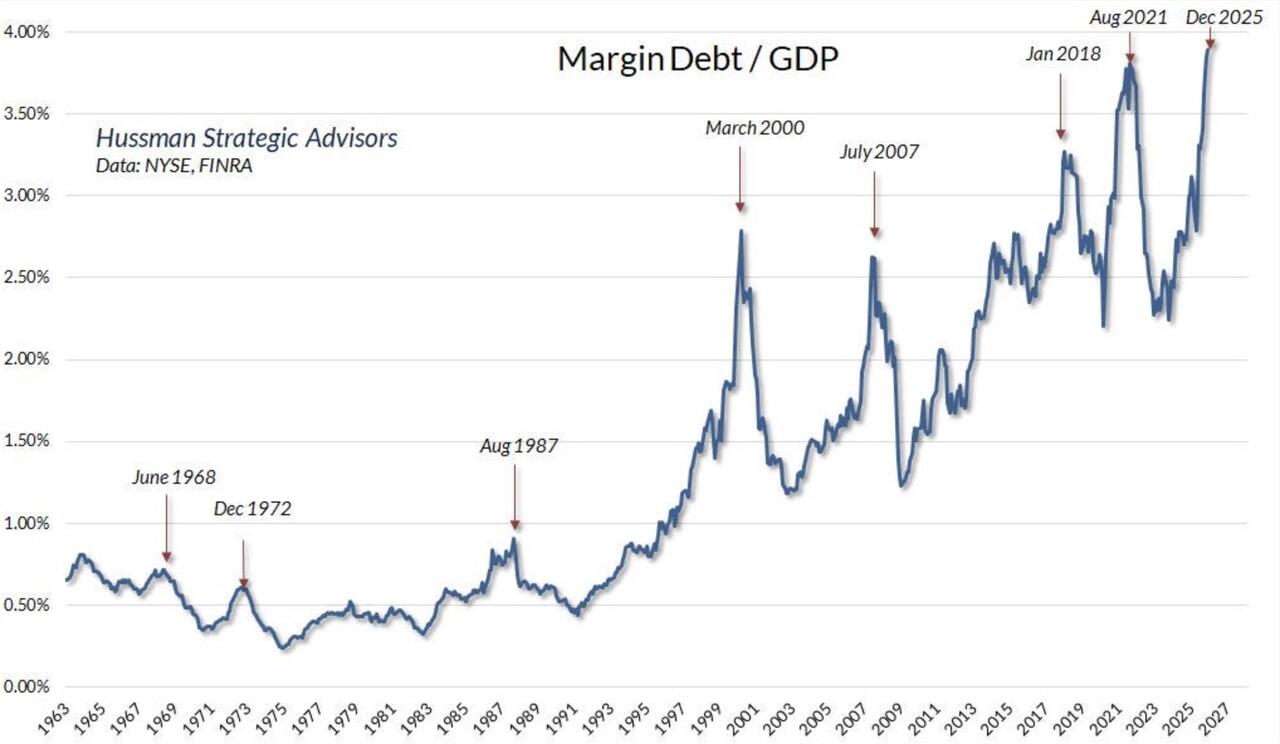

At the same time, leverage and margin debt has expanded throughout the system, and options-driven flows have become an increasingly important source of market support. Dealer gamma effects can suppress volatility on the way up, creating the illusion of stability.

The problem is that the same mechanics can work in reverse.

When positioning begins to unwind, liquidity can disappear quickly. Dealers hedge. Leverage gets reduced. Momentum traders head for the exits. What looked like a calm staircase higher suddenly resembles an elevator ride lower. And that is usually accompanied by television personalities assuring viewers that everything is perfectly healthy.

None of this means we’re headed for a crash. It does mean investors should be careful about assuming every decline is automatically a gift.

🔥 85% Off If You Subscribe To Fringe Finance Today. This coupon allows for 85% off of annual subscriptions and results in a 89% savings over paying the monthly rate for a subscription to the blog. You keep the discounted rate for as long as you wish to remain a subscriber: Get 85% off forever

That mindset worked exceptionally well when valuations were lower, liquidity was abundant, and the Fed was eager to rescue markets at the first sign of distress.

Those conditions do not exist today. A 3% selloff is not a valuation reset. Bitcoin falling is not necessarily an isolated event. And a market priced near historic extremes with a Fed constrained by inflation is not the same environment investors enjoyed during most of the post-2008 era.

The market has temporarily remembered gravity exists. The question now is whether investors will remember it too. If they do, hold on to your nuts, cause I feel like it won’t take much for us to be on the verge of a leverage fueled sell-off that could reinvent our idea of “sharp correction” faster than you can say “subprime is contained”.

Now read:

- Semiconductors Are The “Shitco” Sector: Harris Kupperman

- Bitcoin Bulls All Have A Breaking Point

- This SpaceX Pump Just Keeps Getting Uglier

- Walking Away

- Lest We Forget, Private Credit Is Still Imploding

- Morningstar Just Issued The Most Bearish SpaceX Valuation Yet

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions.

As of May 20, 2026 I personally no longer actively trade (read my story here). My investing/saving is done by recurring contributions mostly to sector ETFs and a few select equities, trusted third parties who oversee my accounts, and advisors. Such advisors or funds, through individual equities, options, index funds, mutual funds, ETFs, or other securities, may have positions in, exposure to, or holdings of names mentioned herein that I know nothing about. Basically, via index funds, ETFs and individual equities it is possible I could own, have exposure to, or not own anything at any point. As of the same date, May 20, 2026, in an attempt to lead a healthier lifestyle, I’ve also excluded myself from fantasy sports, sports betting, online and in-person casinos and prediction markets.

And all positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Tyler Durden

Sat, 06/06/2026 – 11:40

ZeroHedge News

[crypto-donation-box type=”tabular” show-coin=”all”]