Gold Waits As Global Markets Tempt The Unprepared

Authored by Matthew Piepenburg via VonGreyerz.gold,

2026 is screaming “Uh-Oh” signals from nearly every sector and asset class with alarming yet eerily ignored clarity. This explains why the longer-term case for gold couldn’t be more obvious, regardless of natural price retracements in the near-term.

In fact, if global financial conditions were not otherwise so disturbing, this historical moment in time would be fascinating.

But rather than just say this, let me show you.

Rising Yields: The Most Misunderstood/Important Signal of 2026?

For example, the $145T global bond market, which is $20T greater in size than the global stock market, remains less understood yet far more significant as an indicator.

Specifically, this “boring” bond market is foretelling an historical sovereign debt crisis which is already playing out before way too many closed eyes.

Yields on sovereign IOUs (British, American, German, Italian, Japanese, etc.) are climbing to the highest levels seen in decades.

Three Reasons/Warnings for Rising Yields

These yields rise when demand, price and, of course, TRUST in government bonds tank.

This dying trust has a lot to do with global debt levels at over $360T and U.S. public debt levels reaching an embarrassing $40T marker, which effectively makes America one big “bad credit.”

(1) Lenders Demand a Risk Premium

Those with bad credit, of course, are charged a higher risk premium or “yield” by lenders, which explains why the yield on the U.S. 10Y has risen by 75 basis points in a matter of months despite a Fed which has yet to raise rates in 2026.

The Fed, alas, is openly losing control of its bond market. This matters, because rising yields mean rising debt costs, which debt-addicted and debt-driven nations like the USA simply can’t control or afford anymore.

(2) More Buyers than Sellers of USTs

In addition to its fall from credit grace, the home of the world reserve currency and once sacred “return-free-risk” 10Y UST is watching helplessly as former buyers of its critical IOUs are rapidly becoming sellers—a force which just sends those fatal yields even higher.

China, for example, once held over $1.3T in USTs. Today it holds less than $650B. Japan, the world’s largest holder of U.S. debt, just sold more USTs in Q1 of 2026 than it has sold in the last four years.

(3) The Brutal Math of Debt

But the most obvious reason for the dumping of American bonds boils down to just brutal math.

Uncle Sam, which is now running an unsustainable 7% current account deficit, is adding $2.5T of new debt to its banana republic balance sheet per year. America spends 50% of its annual tax revenue just to pay interest on its outstanding debt.

Trillions more in unfunded liabilities are also owed, for which the USA simply does not have the funds.

To fill this income vs expense “gap,” it’s no great mystery that this can only be done with trillions more debased, “mouse-clicked” fiat dollars.

This extraordinary (and increasing) dollar-dilution direction explains why the DXY can’t break 100 despite spiking yields.

Gold and a Little Bit of History Repeating Itself

The slow yet steadily increasing death spiral of fiat currencies is fascinating, obvious and yet totally ignored by current stock chasers—at least for now.

It is also a perfect set-up for gold, which the world continues to ignore based on recent and short-term price action rather than longer-term preparation or historical understanding.

The fake liquidity now and to come to “solve” the above bond crisis is an almost mirror image of the 1970-1980 era, when the Dollar lost 50% of its purchasing power, and gold went from $35 to $850 an ounce.

But like the current bull run in gold, the template of the 1970s didn’t happen in a straight line, as midway through that infamous decade, gold saw sell-offs which shook out speculators yet made longer-term investors generational wealth.

The recent price declines in gold are thus no surprise within a secular bull cycle.

As explained elsewhere, gold’s value, liquidity and prominence have been confirmed by forced sales (from sovereigns to fund managers) to create needed liquidity in times of stress.

Such behavior confirms rather than detracts from gold’s rising profile and prominence in the years and cycles to come.

Nevertheless, many are understandably following traditional thinking that a “yield-less pet rock” is less impressive than a high-yielding sovereign bond.

But bonds are only “high-yielding” because they are unloved, distrusted and broken; the only way to “fix” them, moreover, is by debasing the very currency used to measure their so-called “higher” yields.

Such logic misses the currency-weak forest for the higher-yielding trees.

But as figures like Charles Mackay or John Hussman have so often reminded us, “logic” goes out the window when tech stocks and market meme manias replace basic common sense, sound valuation or even a mediocre grasp of history.

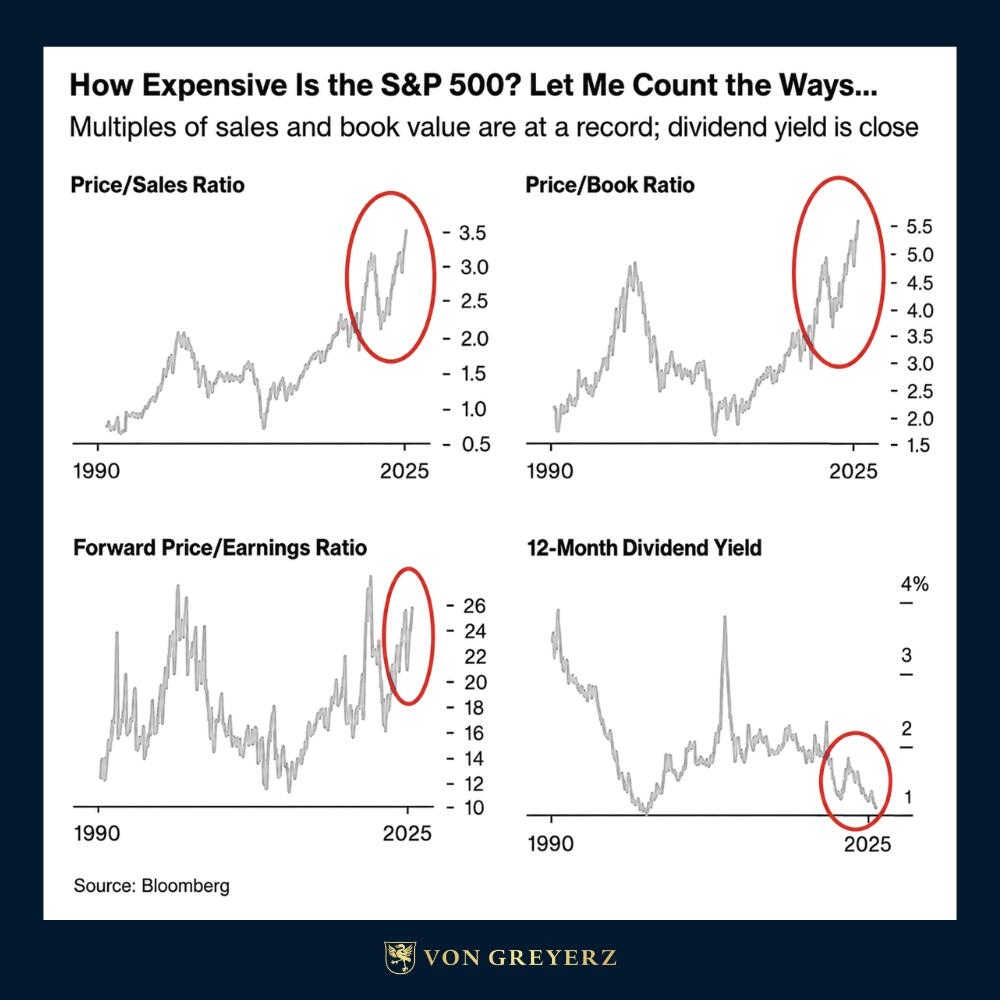

Meanwhile: Stocks Defy Sanity, Valuation and Common Sense

Looking at the current U.S. stock market is like looking at a bad, surrealist film with a cheap laugh-track.

By literally every metric, the S&P is grotesquely overvalued:

Investors are currently paying maximum prices for unprecedented valuation risk and historically minimal dividend income.

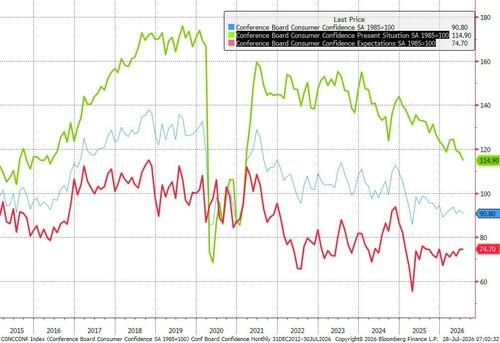

That’s not logic. It’s madness. As consumer sentiment tanks to the lowest levels recorded at the University of Michigan, and as U.S. credit card delinquency rates climb past 12%, the S&P smiles…

Lead to Temptation

As usual, the Wall Street whales and their Sirens on the rocky shores of the equity and credit trap are seducing the retail plankton to their cyclical doom—pumping stocks on the backs of suckers before the big boys take profits on the eve of a fall.

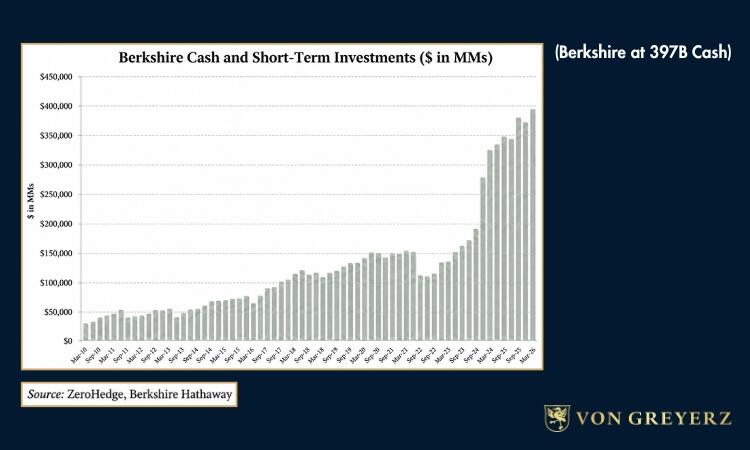

Of course, the infamous “Buffett Indicator”, which measures equity market cap against GDP, has never been clearer (or higher) in confirming such risk:

But the far more telling “Buffett Indicator,” in my mind, lies in the simple fact that Berkshire Hathaway is sitting wisely in nearly $400B in cash.

Alas, the Oracle of Omaha is openly getting out of harm’s way as legions of retail investors march toward an equity cliff.

The tragedy of the so-called S&P 500 (led by 10 stocks) is that it is really no stock market at all. Instead, it lives and breathes off the moral hazard notion that bad news is good news, as there is always a firehose of Fed liquidity (printed dollars) waiting to “accommodate it.”

Every dip is now perceived as a prelude to a V-shaped recovery compliments of the Federal Reserve, which is neither “Federal” nor a “reserve.”

From Temptation to Lying

But such a dishonest title is no match for the dishonest wordsmithing for which the Fed is now so infamous, whether in denying a “non-recessionary recession,” a growing rather “transitory” inflation trend, “non-QE QE” or just flat out lying about actual vs “reported” inflation.

In fact, the Fed’s desperate yet consistent policy of using dishonest words to buy time, markets and votes while hiding honest math will only continue under Kevin Warsh, a trend which he has all but openly confessed.

In case you haven’t noticed, Warsh intends to measure PCE inflation under a new metric called “trimmed mean PCE,” which effectively removes all the bad inflationary data to create a fictitious notion that inflation is under control.

This is duplicity at its finest. After all, even a witch can look pretty if you take away the warts, which is all Warsh’s new Fed policy boils down to.

In fact, what Warsh is doing is nothing surprising nor anything new.

The Oldest & Only Trick Left: Inflate Away Debt

While the rest of us endure the invisible theft of compounding inflation, the policy makers in DC will secretly welcome it as a means to inflate away their sovereign bar tab on the backs of your purchasing power and wealth.

This is called “negative real rates” or “financial repression,” and it’s the oldest trick in the book of desperately broke nations, namely: Let inflation rip higher than interest rates, but then lie about the embarrassing inflation.

When Even the Official Math is Bad

What’s as disturbing, however, is that even the “official” inflation data, as dishonest and downplayed as it is, is still alarming evidence of open monetary policy failure.

Current U.S. CPI inflation (the cost of consumer goods) is racing past 3.8%, and current U.S. PPI inflation (the business cost of making goods) is already at an embarrassing 6%–well beyond the Fed’s 2% “targets.”

But this is just the beginning. Since the Strait of Hormuz closed, the cost of fertilizer has risen by 20%, gasoline by 52%, European natural gas by 54%, jet fuel by 58%, and WTI crude oil by 60%.

Yet how can U.S. CPI and PPI inflation be in the single digits when everything else has risen by massive double digits?

Well, be patient, because the inflationary lag effect of this “conflict” in Iran (whatever you think of it) is racing toward your shores at an increasing wave height.

From Inflation to Gold: Keep it Simple

These inflation signals, as well as the bond signals above, and the stock mania already covered, are all just flashing neon-indicators of surreal “Uh-Oh” in the risk asset markets and an historical moment of currency debasement in your wallets and homes.

This is not fable but tragic fact.

Gold, whatever its current price, is positioning itself for a lengthy, secular and historical move north. It has a finite supply and infinite duration and is thus far more honest than the unlimited supply and finite duration of sovereign bonds and paper currencies.

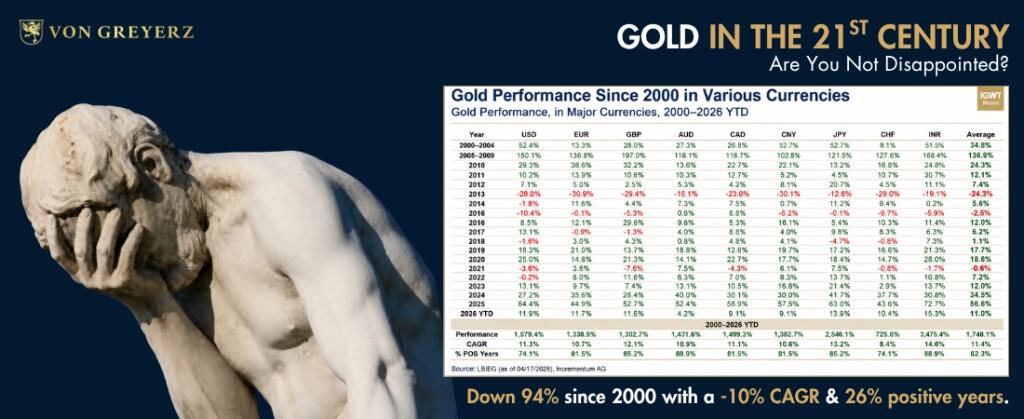

For those who still think gold has not done enough, compare its recent history here:

…to the same history of global paper currencies here:

It’s really just that simple.

Gold will continue to climb because a global paper currency system distorted by decades of debt, dishonesty, desperation and debasement has nowhere to go but down.

For wealth preservation investors who understand the math of bonds and the history of debt, this simplicity provides for clarity in a time of fog, sanity in a time of madness, and wealth protection in a time of wealth destruction.

Tyler Durden

Sun, 05/31/2026 – 11:40

ZeroHedge News

[crypto-donation-box type=”tabular” show-coin=”all”]