Bank Of Canada Warns Markets More Vulnerable To Sharp Correction Due To AI Concentration, Basis Trades

The Bank of Canada said the global financial system has functioned (surprisingly) well through recent global shocks, but underscored the risk of a sharp asset price correction as well as vulnerabilities related to the role hedge funds are playing in debt markets.

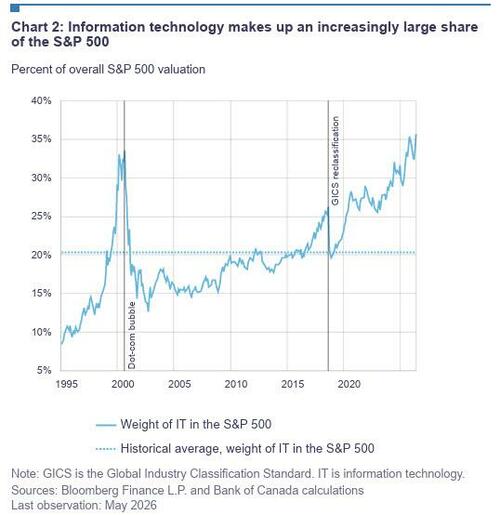

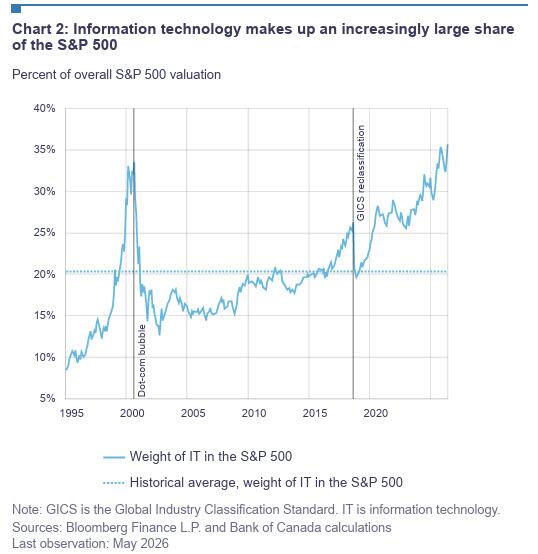

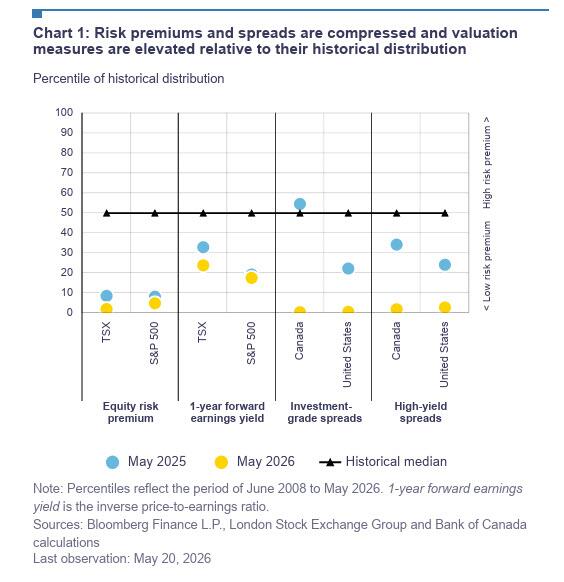

The central bank’s 2026 financial stability report released Thursday noted financial asset valuations have continued to rise, while the stock market is increasingly concentrated in a handful of large tech companies that are heavily invested in artificial intelligence. That makes asset managers more vulnerable to a sudden correction, and a negative shock to AI sectors would have an outsized impact on broader stock indexes.

The central bank also reminded markets that the risk of basis trades remains front and center, warning that the increased role of hedge funds in overnight funding markets poses a vulnerability to the overall financial system, Bloomberg reported.

“A sharp pullback in hedge fund activity in government debt markets, for example, could negatively affect the liquidity and functioning of these markets and other fixed income markets. This, in turn, could generate financial system stress,” the report said.

While senior Deputy Governor Carolyn Rogers said individually, these vulnerabilities look “manageable”, he added that “the economic and geopolitical environment has become more volatile. And this has made it more likely that a new shock or a combination of shocks could cause several vulnerabilities to crystallize at once.”

The report analyzes risks to the Canadian financial system, but doesn’t assign probability and isn’t a projection from the central bank.

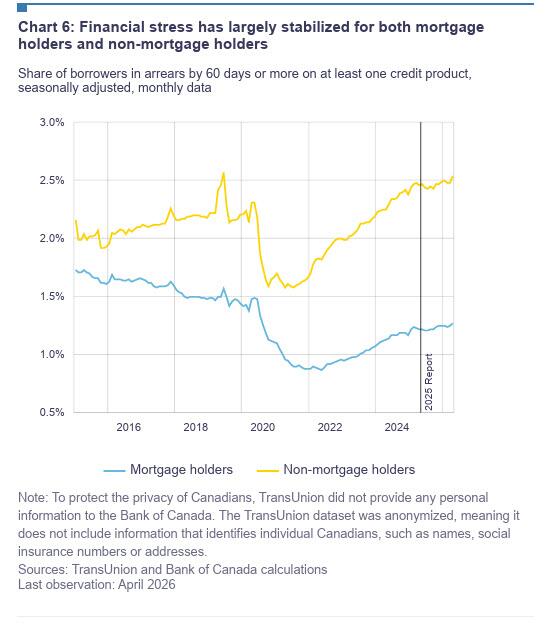

Meanwhile for households and businesses, the bank said the main financial health vulnerability relates to a geopolitical or economic shock that leads to a deep recession and a spike in unemployment. While the central bank previously flagged mortgage renewals as a concern, it noted on Thursday that most borrowers have managed this risk well.

“With the final wave of these renewals set to happen over the next 12 months, we expect this risk to have fully passed by the second half of 2027,” Deputy Governor Toni Gravelle said.

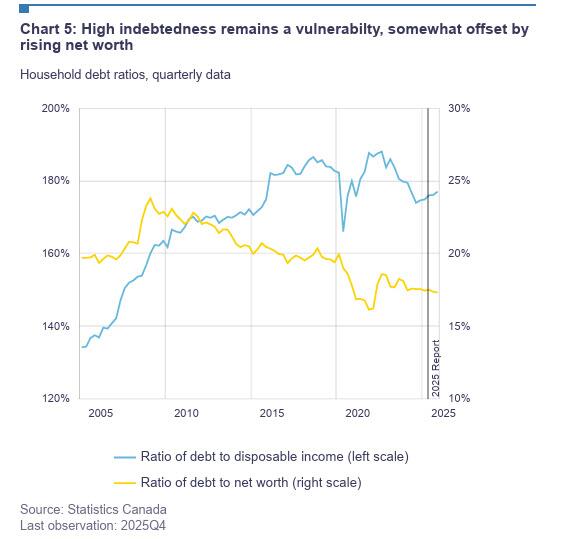

While the ratio of household debt to disposable income has increased slightly over the past year, the central bank noted households appear better off when wealth is taken to account.

It attributes that improvement to higher home prices over time, but noted the recent increase in net worth has been driven by gains in financial markets as the housing market softened.

As for Canada’s big banks, the report says they have become more resilient over the past year amid higher profitability and healthy capital buffers.

“They have also set aside additional funds to absorb potential loan losses. This positions them to support the economy and financial system, even in a severe downturn,” Gravelle said.

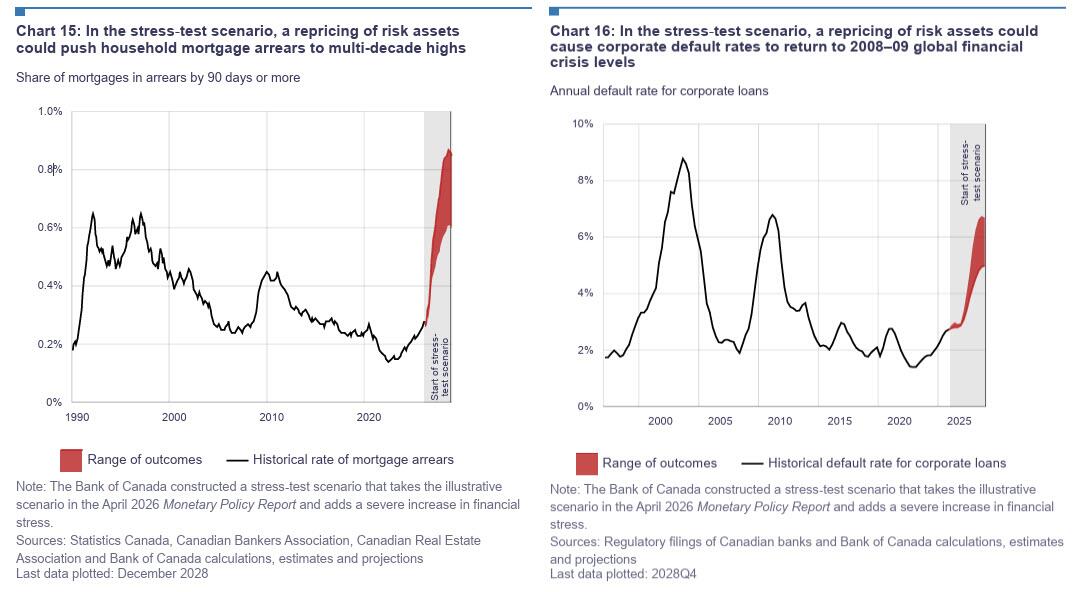

The report cautioned that in the stress‑test scenario, as unemployment rises and housing prices fall, households and businesses come under significant stress. Rates of mortgage arrears increase and reach a multi‑decade high. Businesses face increased costs and a decline in demand, which pushes corporate default rates close to levels seen during the global financial crisis.

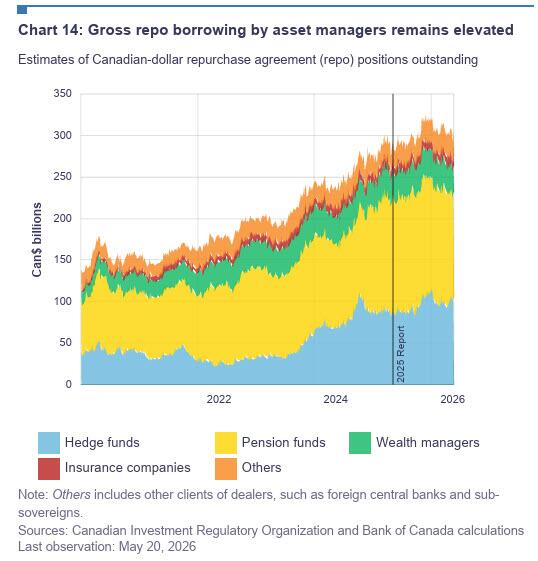

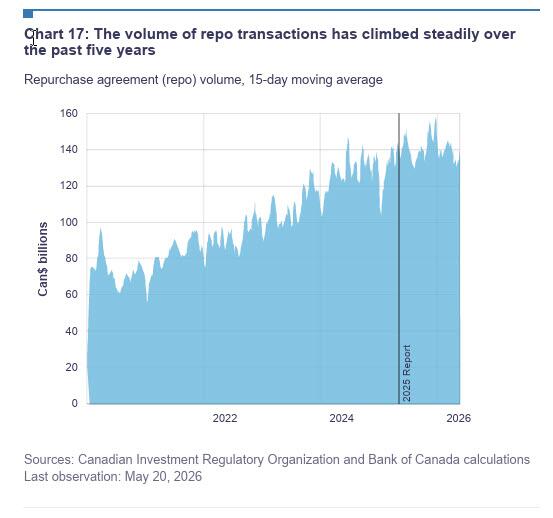

Meanwhile, the aggressive use of repo markets has further increased their importance in Canada’s financial system. More than $130 billion in repo transactions now take place in Canada each day, about double the amount from five years ago. A wide range of market participants use repos to obtain leverage, borrow and lend securities, earn returns on extra cash and manage funding liquidity.

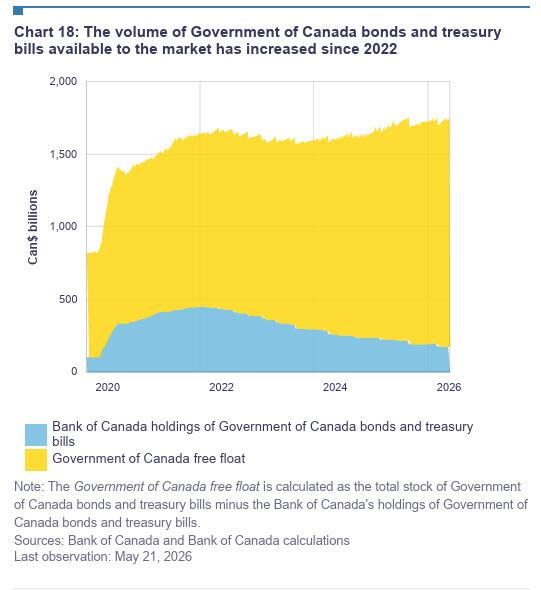

The report cautioned that repo activity is rising in part because more Government of Canada bonds are being issued and traded.

Repos are a flexible and cost‑effective way to finance trading in government bonds and therefore play an important role in facilitating dealers’ market‑making activities. They also allow hedge funds to finance their activities, including basis trades in government bonds and futures. These activities, in turn, support liquidity and efficiency in the markets for government securities.

Government bonds are widely used as collateral and liquid assets to manage risks. They are also used as pricing benchmarks for other securities. Because of this, a disruption in repo markets would have broad implications for the financial system. These include:

- A sudden deleveraging by asset managers. For example, if hedge funds or other asset managers cannot obtain repo funding, they may need to quickly sell government bonds, further reducing market liquidity.

- A reduction in overall market liquidity. Wider bid‑ask spreads and higher trading costs in government bond markets could spill over into other fixed‑income and derivative markets. If this led to significant margin calls, it could result in a liquidity spiral as market participants are forced to sell liquid assets to raise cash.

- Sharp movements in the Canadian Overnight Repo Rate Average (CORRA). This would affect the large numbers of financial instruments that use CORRA as a risk‑free rate, such as interest rate derivatives and floating rate notes.

The report concludes that if any of these situations were to occur, “borrowing costs across the economy would go up, leading to potential second‑round effects.”

Tyler Durden

Thu, 05/28/2026 – 12:00

ZeroHedge News

[crypto-donation-box type=”tabular” show-coin=”all”]