One Key Signal Says Rate Hikes Could Be Coming

Submitted by QTR’s Fringe Finance

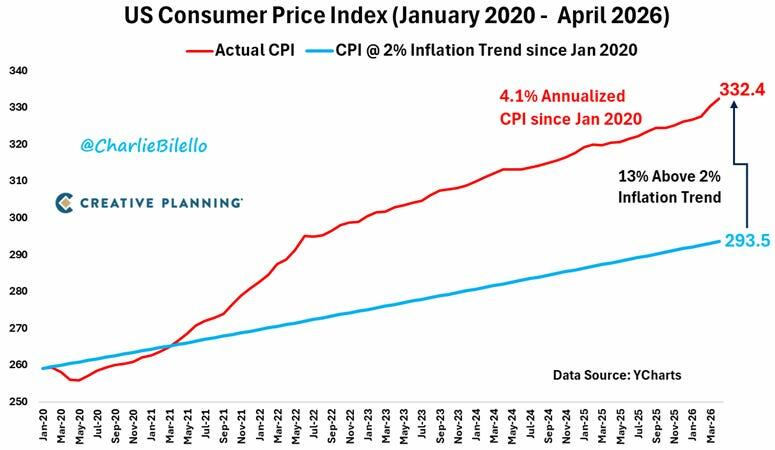

For a while now markets have operated under the assumption that inflation was cooling, rate cuts were inevitable, and the Federal Reserve was slowly steering toward a soft landing. Hell, Jim Cramer started celebrating Jerome Powell’s “soft landing” some 925 days ago with inflation at 3.1%. Today, inflation is at 3.8% and Powell is leaving his post at the Fed and turning over his impossible task to Kevin Warsh.

Which is to say the consensus is starting to unravel fast. Treasury markets are repricing aggressively, Fed officials are openly acknowledging hikes are back on the table, and fresh inflation data continues coming in hotter than expected.

And it is now being reported that one of the bond market’s most closely watched signals continues to point to a higher-for-longer policy, and potentially another rate hike cycle altogether. More importantly, this is exactly the shift I warned about days ago when I argued the “cuts only” narrative was beginning to crack under mounting inflation pressure.

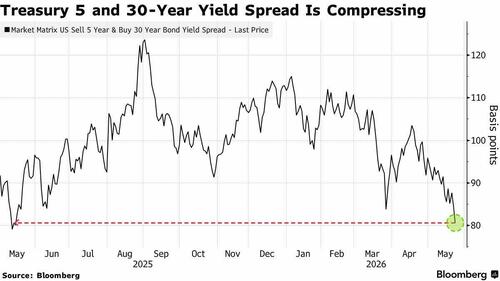

Bloomberg’s latest reporting reinforces the exact shift that markets have been slowly waking up to over the last several weeks: the bond market is no longer confidently pricing a clean disinflationary path toward lower rates. Instead, Treasury markets are beginning to price the possibility that the Federal Reserve may need to stay restrictive — or even tighten further.

As Bloomberg’s Ruth Carson reported, one of the clearest signals of this shift is happening inside the Treasury curve itself. The spread between 5-year and 30-year Treasury yields tightened to its narrowest level in roughly a year, briefly hitting 81 basis points before slightly rebounding. Bloomberg notes this move reflects investors repricing the likelihood that rates remain elevated for longer under incoming Fed Chairman Kevin Warsh.

Importantly, Bloomberg emphasizes that the flattening is being driven primarily by pressure on shorter-duration Treasuries, which are far more sensitive to changing Fed expectations. In other words, traders are aggressively repricing the front end of the curve higher because they increasingly believe the Fed may not only abandon cuts, but could eventually be forced back into hikes.

As Bloomberg wrote:

“The data and the politics are suggesting less pressure for rate cuts, and short-end yields have been repricing higher,” according to Nomura strategist Andrew Ticehurst. Bloomberg also highlighted that Fed Governor Christopher Waller — previously viewed as more dovish — recently said the Fed’s next move is now “just as likely to be a hike.”

That is a remarkable shift in tone compared to where markets stood only months ago.

The piece further points out that traders are now pricing roughly an 80% probability that the Fed begins raising rates again by December — a dramatic reversal from the pre-Iran-war consensus, when markets were still expecting multiple cuts this year.

It notes that strategists across major institutions including ING, Goldman Sachs, and Barclays increasingly believe structurally higher yields may persist even if energy prices cool, due to massive fiscal deficits, defense spending, AI infrastructure investment, and sticky inflation pressures.

The broader message is that the Treasury market itself is beginning to flash warning signs that inflation risks are reasserting themselves and that the Fed may be losing the flexibility markets previously assumed it had.

What makes this especially notable is that it aligns almost perfectly with the argument I laid out several days ago.

I argued then that the “rate cuts are inevitable” narrative was beginning to crack under the weight of reaccelerating inflation data. The key point was not simply that inflation remained elevated, but that the underlying trend was moving in the wrong direction at precisely the moment markets had become heavily positioned for easing.

At the time, I highlighted two major developments:

-

CPI remained materially above the Fed’s 2% target, coming in hotter than expected at 3.8%.

-

PPI delivered an even larger upside surprise, with wholesale inflation surging 1.4% month-over-month and 6% annually — the strongest increase since 2022.

The significance of those reports was that they challenged the market’s assumption that inflation was steadily cooling toward normalization. Producer prices in particular matter because they often act as an early pipeline indicator for future consumer inflation. Rising input costs tend to bleed into the broader economy over time.

I also pointed out that Fed officials themselves had stopped dismissing the possibility of tighter policy. Austan Goolsbee explicitly stated that “all options remain on the table,” while warning that inflation pressures extended beyond temporary energy shocks. At the time, markets had already started repricing rate-cut expectations and were beginning to assign meaningful odds to another hike.

🔥 90% Off If You Subscribe Today. This coupon allows for 90% off of annual subscriptions and results in a 90%+ savings over paying the monthly rate for a subscription to the blog. You keep the discounted rate for as long as you wish to remain a subscriber. I will not be offering 90% off anytime again soon after the long weekend: Get 90% off forever

Now, only days later, Bloomberg is documenting the same repricing process accelerating inside the Treasury market itself.

That consistency matters because the bond market tends to lead broader macro realization cycles. Yield-curve flattening driven by rising short-end yields is not what you see when investors are confidently expecting imminent easing. It is what you see when markets begin preparing for policy staying restrictive longer than anticipated — or potentially tightening further.

My broader thesis remains unchanged: The Fed is trapped between two deeply unattractive outcomes. If policymakers hike rates again into a reaccelerating inflation backdrop, they risk detonating highly leveraged parts of the economy that have survived largely because of years of ultra-cheap money. Speculative assets, private credit, subprime lending, and risk-heavy corners of the market become vulnerable very quickly in that environment.

But if the Fed backs away from tightening because markets or growth weaken, they risk reigniting another inflation wave by reverting back toward liquidity support and easier policy before inflation is actually contained.

That is why the conversation has shifted so dramatically in such a short period of time. What looked like a fringe scenario months ago is increasingly being treated as a legitimate macro risk by bond traders, Fed officials, and major Wall Street institutions alike.

And the Treasury market is now starting to reflect that reality in real time.

—

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions.

As of May 20, 2026 I no longer actively trade (read my story here) and my accounts are managed by recurring contributions to trusted third parties and advisors and/or recurring contributions mostly to sector ETFs. Such advisors, through individual equities, options, index funds, mutual funds, ETFs, or other securities, may have positions in names that I know nothing about. Basically, I could own or not own anything at any point, and not have any idea about it.

And all positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Tyler Durden

Wed, 05/27/2026 – 13:00

ZeroHedge News

[crypto-donation-box type=”tabular” show-coin=”all”]