Fed-dling While “Rome” Churns

By Michael Every of Rabobank

The Bank of Canada cut its policy rate 25bp to 2.50% as expected, largely attributing its decision to softer CPI data, a loosening labour market, and a more optimistic inflation outlook given PM Carney’s decision to repeal retaliatory tariffs on US goods. We are forecasting another 25bp cut in October and see the terminal rate at 2.25%. However, the risk to our view is skewed in favour of two more cuts this year over none. (See here for our full report.)

The Fed decision was also in line with expectations with a 25bp cut to 4.00 to 4.25%. (See here for our report.) There had been speculation as to whether the meeting would be riddled with dissent, but it only stemmed from new joiner Miran’s call for a 50bp move. The key takeaway from the accompanying statement was that “the Committee is attentive to the risks to both sides of its dual mandate…downside risks to employment have risen”. That said, Powell stated the -911K change in payrolls through to March 2025 was “almost exactly” what the Fed had expected. That’s either a good forecast or convenient given the Fed didn’t look like it saw it coming.

Looking ahead, the ‘dot plot’ averages a Fed Fund rate of 3.6% by end-2025 and 3.4% by end-2026, -0.3 and -0.2 from June, respectively. However, one board member is forecasting a 2025 year-end implied rate of 2.88, which would suggest 50bps cuts at the October and December meetings. Some are speculating this may be Miran, but that cannot be proven. When pressed, Powell replied that “a wide range of views is natural in the current situation.” We now forecast another 25bp cut at the October 29 meeting, and still see a terminal Fed Funds rate of 3.00%.

In the press conference, Powell had to deal with a battery of more political questions: one wonders if this is going to be something we see more regularly.

Notably, Powell’s tone and the FOMC statement was initially interpreted as dovish, invoking a 9bp dip in 2-year Treasury yields and 6bp in the 10-year. However, 10s ended higher on the day along with the 5Y-5Y forward inflation swap, pointing to rising inflation expectations as the Fed cuts into a stagflationary-esque environment. In the FX market, pre-Fed, the FT noted, ‘Foreign investors in US assets rush for protection against swings in dollar’, with a “sharp increase in hedging” amid a “broad rethink on exposure” – but USD dipped then rallied.

This Fed-dling of course took place as ‘Rome’ churns, rather than burns. Indeed, aside from political drama in D.C., in geopolitics:

The EU is reportedly to explore using €170bn of Russia’s frozen assets to fund Ukraine, and though some European capitals remain wary over a ‘reparation loans’ plan, the US is apparently also calling on the G-7 to do so. Recall the US took half of Afghanistan’s FX reserves in 2022 and some of Iraq’s in 2003, Iraq seized Kuwait’s in 1990, and the Nazis Czechoslovakia’s gold in the 1930s – but nothing has been done on this kind of scale before. It could jump start more discussion of diversification from the dollar and euro… but into what exactly?

That’s as US Senator Graham told Hungary and Slovakia to stop buying Russian oil –“I hope and expect them to step up to the plate soon to help us end this bloodbath. If not, consequences should and will follow.”—while the Wall Street Journal, in ‘Putin’s Polish Drone Incursion and the China Factor’ asks “Is the war in Ukraine being prolonged primarily to serve Beijing’s interests?”

The EU set out plans for partnership with India on trade, technology, security, defence, and climate, also including the India–Middle East–Europe Economic Corridor (IMEEC). However, as The Hindu notes, “India’s military exercises with Russia and its continued purchase of Russian oil are seen in Brussels as potential obstacles to the deepening of the relationship with New Delhi.”

Moreover, if the EU strikes a deal with India, it likely presages a US-India deal alongside it, not only in tariff and transshipment terms, but due to the IMEEC. Indeed, with Trump and PM Modi exchanging warm public greetings as the latter turned 75, it once again seems to be when we see US tariffs on India lowered, not if.

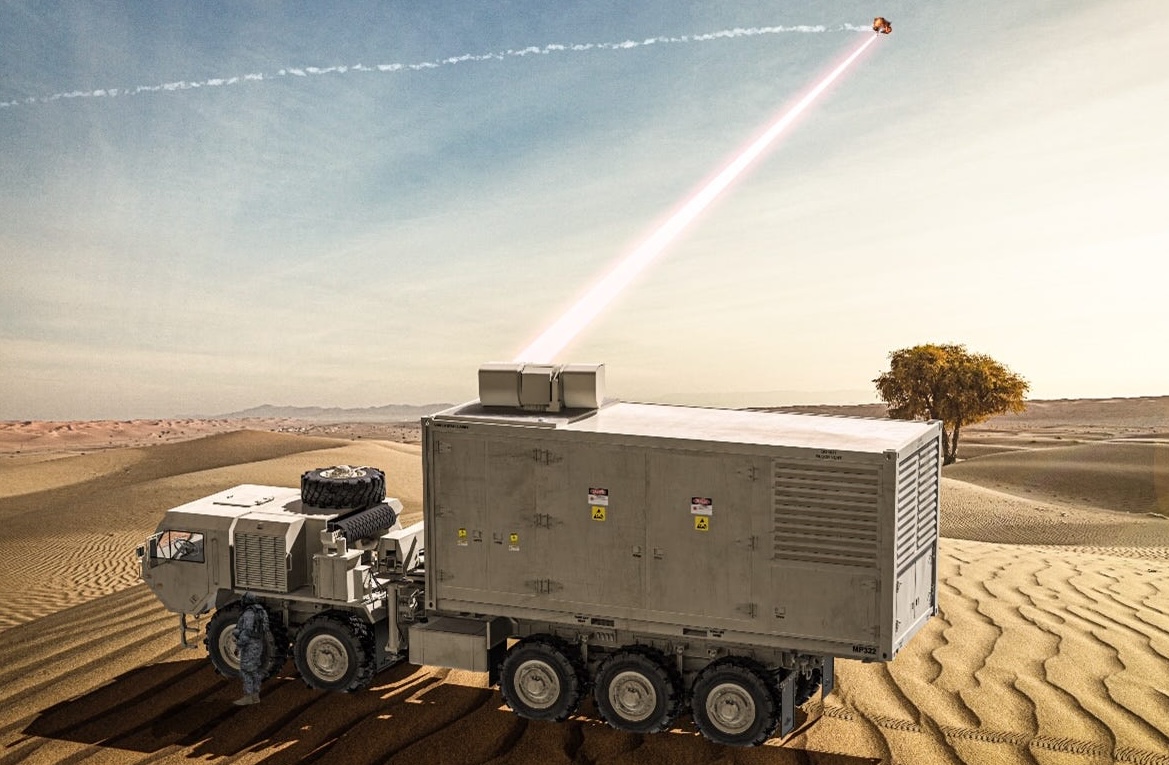

In the Middle East, the EU proposed sanctions and the partial suspension of its trade deal with Israel; just as the latter announced the world’s first laser-based interception system, which could transform the economics of building the defensive shield Europe needs.

Moreover, as the Free Press describes ‘Why Trump Let Netanyahu Strike Hamas in Doha’ (“The US president and the Israeli prime minister have developed a good cop-bad cop routine”) Saudi Arabia signed a ‘strategic mutual defence’ pact with Pakistan, a sign of how rattled it was by the recent Israeli attack on Hamas leaders in Qatar. That underlines the urgency for the US to cement a broader Middle East geostrategic architecture like IMEEC; and that’s as Syria’s President Sharaa said security pact talks with Israel could yield results “in the coming days.”

In geoeconomics: China banned its tech companies from buying Nvidia’s AI chips, as Beijing steps up its efforts to boost semiconductor independence; South Korean manufacturers outlined their plans to bolster U.S. shipbuilding (though the Hyundai plant in Georgia recently raided by ICE reportedly won’t see construction restart until 2026); and US tech giants urged Trump to push back on an Australian tax law they don’t like; and China is pushing for closer Southeast Asia trade links as it fends off US pressure.

In the specific geoeconomic of energy: Abu Dhabi’s Adnoc saw its $19bn bid for Santos fail, keeping a key energy firm in Aussie hands; the USTR is poised to tweak the looming penalty for carrying US LNG on Chinese-built ships as there aren’t enough alternative ships yet, and penalties would push up the price of its energy exports; and Bloomberg asks, ‘Why is China stockpiling so much oil?’ saying it’s “stirring conspiracy theories.” An understanding of statecraft would make clear this isn’t conspiratorial, just logical.

From a broader perspective, the ‘WTO chief finds hope in Trump’s trade disruption, sees chance for ‘reglobalization’ (SCMP). Okonjo-Iweala, acknowledging that global trade is “heavily dented”, nonetheless says the “opportunity is knocking at our door to do things differently”- yet didn’t supply any concrete answers on how to address the “supply imbalances” she admitted the global system currently produces.

From a national perspective — that applies in many places — former Bank of England chief economist Haldane says Labour must rethink its growth strategy “to curb the rise of the far right”, and left-behind communities need investment to stem the populist tide. He also didn’t supply any concrete answers as to how to do it: and his answers and the WTO’s need to join up, as laid out with iron logic by Pettis & Klein in ‘Trade Wars are Class Wars’.

Tyler Durden

Thu, 09/18/2025 – 10:45

ZeroHedge News

[crypto-donation-box type=”tabular” show-coin=”all”]