Debasement: What It Is And Isn’t…

Authored by Lance Roberts via RealInvestmentAdvice.com,

Over the past year, financial headlines continue to flood investors with doomsday predictions about the U.S. dollar.

Whether it’s social media influencers waving “dollar collapse” charts or YouTube personalities warning about debasement, the noise has become deafening. The narrative is seductive: inflation is out of control, the government is printing money, and the dollar is on its last legs. But while there are real risks to watch, most headlines sell fear, not fact.

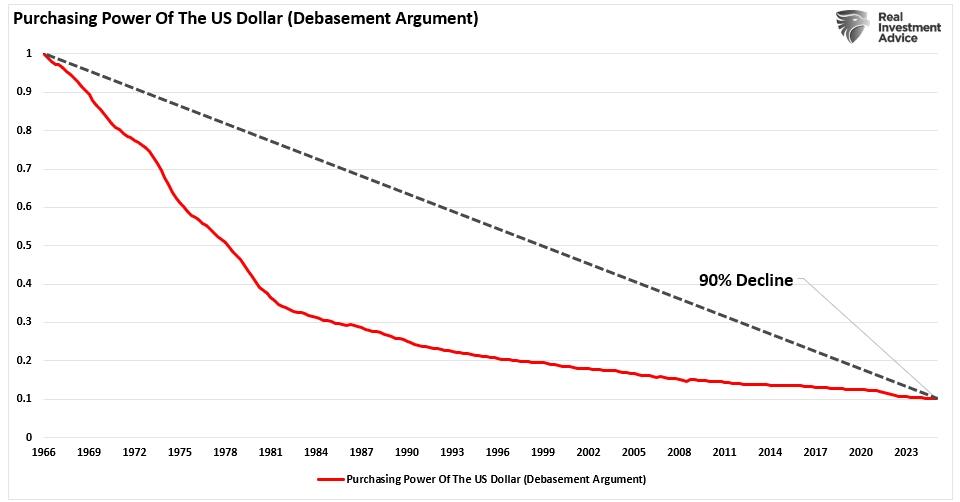

The 90% Purchasing Power Chart: Misleading but Popular

One of the favorite charts used to make the “debasement” case is the classic graph showing that the U.S. dollar has lost 90% of its purchasing power since 1966.

It’s striking, and those selling gold, silver, or other doomsday assets often use it. But here’s the thing: that chart doesn’t show debasement. It only reflects inflation, a well-understood and largely expected outcome in a growing economy.

Prices rise over time because demand increases due to population growth, rising incomes, and growing consumption. This is especially true in a post-industrial, service-driven economy that incentivizes credit expansion and capital investment. As we often say, it’s not the dollar losing value; it’s the economy expanding.

Let’s discuss what “debasement” is and is not as it relates to the economy.

Understanding Inflation vs. Debasement

Let’s start by untangling two often-confused concepts: inflation and currency debasement. While both reduce the purchasing power of a dollar, they operate differently.

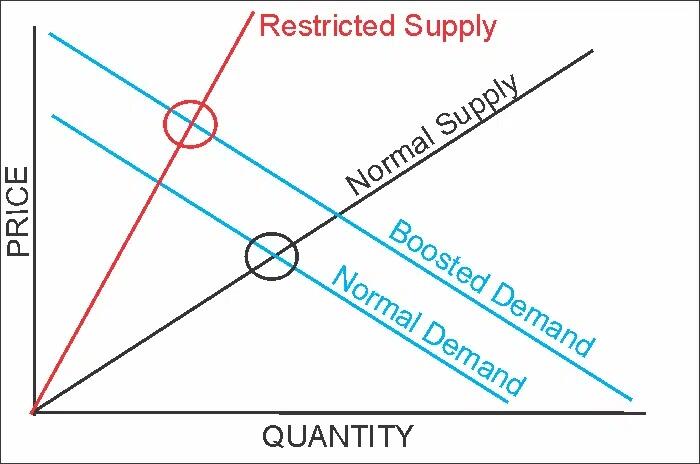

Inflation is the rise in prices due to supply and demand imbalances. Rising wages and consumer demand for products and services that grow faster than the available supply create higher prices (aka inflation). The chart below is from a previous article we wrote discussing why the economy surged following the pandemic-related economic shutdown.

“The following economic illustration is taught in every ‘Econ 101’ class. Unsurprisingly, inflation is the consequence if supply is restricted and demand increases via monetary interventions.”

Conversely, debasement implies a structural dilution of a currency’s value. This is vastly different than inflation. In a “debasement” scenario, governments take conscious actions to reduce the “structure” of the currency. In Rome, for example, the government reduced the amount of silver in minting coins to increase the number of coins produced to pay its creditors. However, debasement is not a reality in a fiat system like ours, where the linkage to gold or silver is nonexistent. In other words, when the government is “printing paper,” it is impossible to dilute the “structure.”

However, the term has become “co-opted” by the bears and fear mongers as a psychological representation of perception and confidence in the dollar. But that is what makes this discussion so interesting. While the “debasement experts” point to record stimulus, growing deficits, and expanding M2 over the last few years, confidence in the dollar remains intact—not just among U.S. consumers and investors but globally.

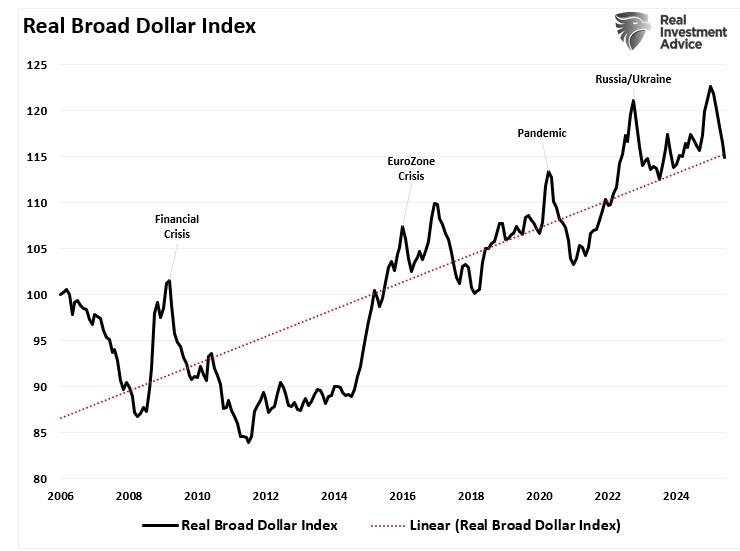

As shown, the U.S. dollar index remains strong. Most notably, the bigger picture reveals a more resilient and globally dominant currency than many alarmists will admit. The U.S. dollar is still at the center of 80% of global transactions, and nearly 60% of all global reserves. The “debasement” argument is at best premature, and at worst, deeply misleading.

But what about that dollar purchasing power chart above?

That chart is not about “debasement,” as shown; it is just a measure of inflation caused by a growing U.S. population and increasing economic demand over time.

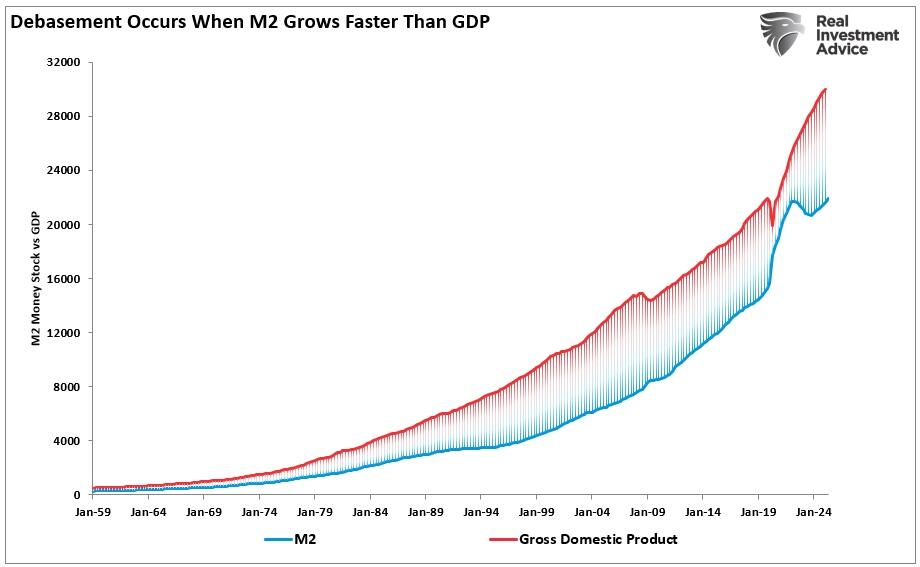

What M2 Growth Tells Us

“No Lance, the dollar purchasing power is going down, because we are printing too much money.”

That would be a fair statement if the Government were increasing the money supply faster than the economic growth rate. In such a case, the surge in the money supply would cause inflation.

We did witness such an event, as the surge in M2 during the pandemic era was unprecedented. During 2020 and 2021, the Government added over $6 trillion to the money supply. But let’s not forget the context: the world was undergoing the most severe economic shock since the Great Depression. The U.S. government and Federal Reserve stepped in forcefully to stabilize the economic and financial system—and it worked. The consequence was, as would be expected, and as shown in the chart above, a shift in the “supply/demand” equation, creating higher prices. However, at the same time, that surge in demand that outstripped supply led to a massive surge in economic growth, sending unemployment to near record lows. That outcome would not have occurred without the increase in the money supply.

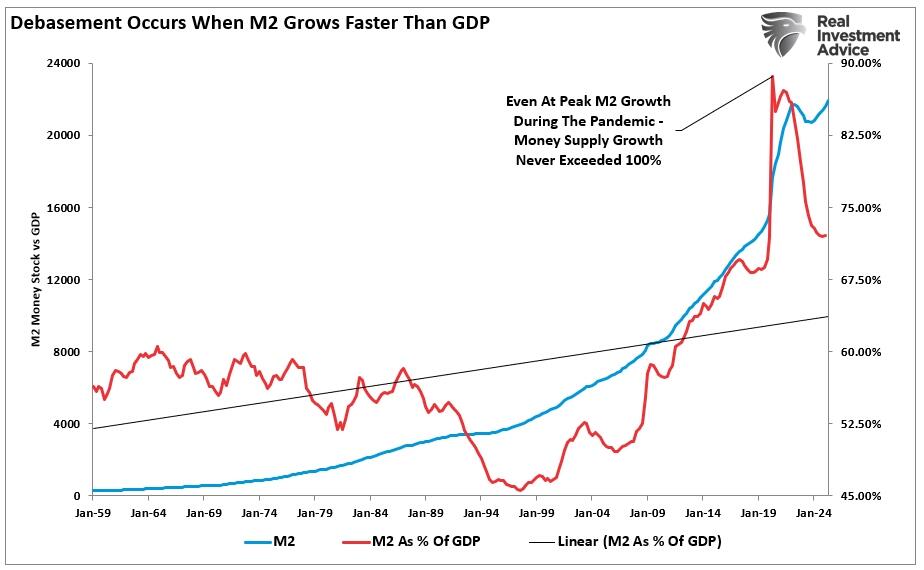

But therein lies the misunderstanding. It’s easy to point to M2 charts and scream “debasement. “ However, the money supply must grow as the economy grows. If it doesn’t, deflationary risks emerge. Therefore, the key is whether money creation exceeds economic growth in a sustained way. Since 1959, the money supply has grown in alignment with economic growth.

A better way to assess this is by comparing M2 to GDP. Historically, the two have tracked closely. Even during the COVID shock, M2 as a percentage of GDP remained below 100%, meaning money supply growth was broadly aligned with economic output. Today, that ratio is falling, not rising.

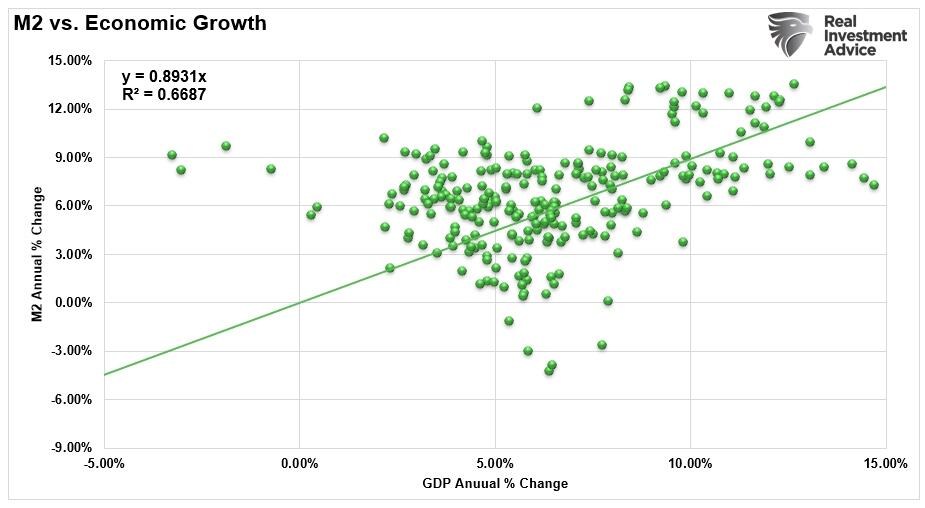

The reality is, as you would expect, that the growth rates of M2 and the economy are highly correlated.

If the dollar were truly being debased, you’d see a very different set of outcomes:

-

Capital fleeing U.S. assets (stocks, bonds, gold, cryptocurrencies)

-

A collapse in Treasury demand.

-

A breakdown in global trade settled in dollars.

Instead, we see the opposite. Treasury demand remains robust. The dollar is still used in 80% of global transactions and represents nearly 60% of international reserves. Central banks, sovereign wealth funds, and institutional investors continue to hold and accumulate U.S. assets.

So, while media pundits scream about a “loss of trust,” global capital continues to support the dollar.

The Dollar’s Death Is Greatly Exaggerated

Every few decades, someone proclaims the end of the dollar. In the 1980s, it was Japan. In the 2000s, it was the Euro. Today, it’s China or crypto. Yet none of these alternatives have been able to replicate what the dollar provides: deep capital markets, rule of law, and the economic and military reach of the United States.

The dollar remains the cleanest dirty shirt in the global laundry basket. That’s not to say it’s perfect, but perfection isn’t the benchmark. Trust, liquidity, and legal protections are. Furthermore, gold, often touted as the “real money” alternative, is traded and valued in dollars.

In reality, “debasement” isn’t the issue that investors should pay attention to. However, “inflation“ over time erodes the purchasing power of dollars. As such, investors must ensure their “savings” grow at the inflation rate over time. That means investing your savings in assets that grow faster than the inflation rate over the long term. We discussed this topic in “Conviction and How to Lose a Lot of Money.”

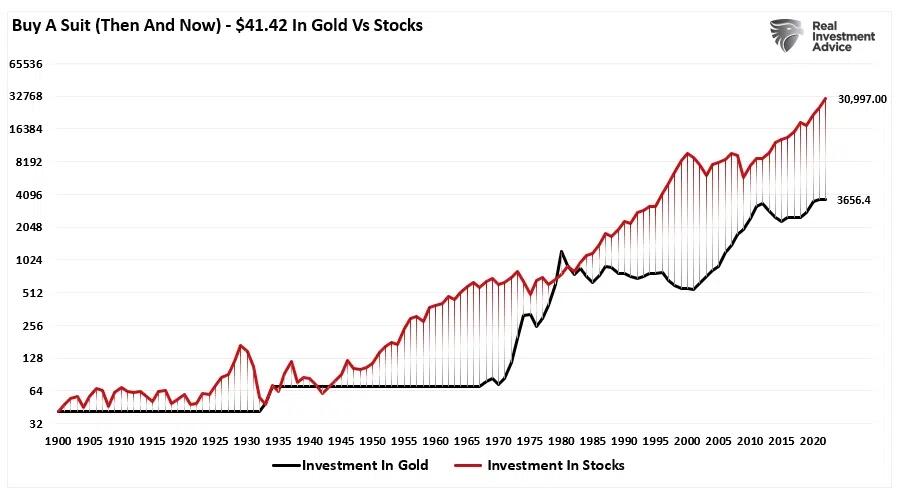

“As an example, let’s consider a high-end men’s suit. In 1900, the average price of a high-end men’s suit was around $35. Today, the average price of a high-end suit is around $2,000.

Looking at it another way, if you had stuffed $41.34 under your mattress in 1900, today you might be able to buy a couple of Polo shirts if you find a deal. But if you had bought two 1-ounce gold coins and stuffed those under your mattress in 1900, today you’d be able to buy a fancy suit and have about $1,600 left over.“ – Michael Maharrey

He is correct in his math. However, the same investment in the stock (price appreciation only since gold doesn’t pay a dividend) allowed an individual to buy 15 suits with money left over.

Yes, gold has been a good hedge against inflation over the long term. Investing in the stock market has been much better.

So why do dollar debasement stories get so much attention? Because fear sells. Human psychology is wired to respond more strongly to threats than to opportunities. This “negativity bias” helps explain why bearish content generates more clicks, listens, and views. It’s not that the content is wrong, but it’s often disproportionately amplified.

Unfortunately, many investors confuse loud narratives with likely outcomes.

For investors, the key takeaway is to separate noise from narrative. While inflation, fiscal deficits, and policy missteps are worth our concern, the U.S. dollar remains the backbone of the global financial system, not because it’s flawless, but because there is still no viable alternative.

Again, “debasement” isn’t the concern it is being made out to be.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of ZeroHedge.

Tyler Durden

Fri, 08/01/2025 – 12:20

ZeroHedge News

[crypto-donation-box type=”tabular” show-coin=”all”]